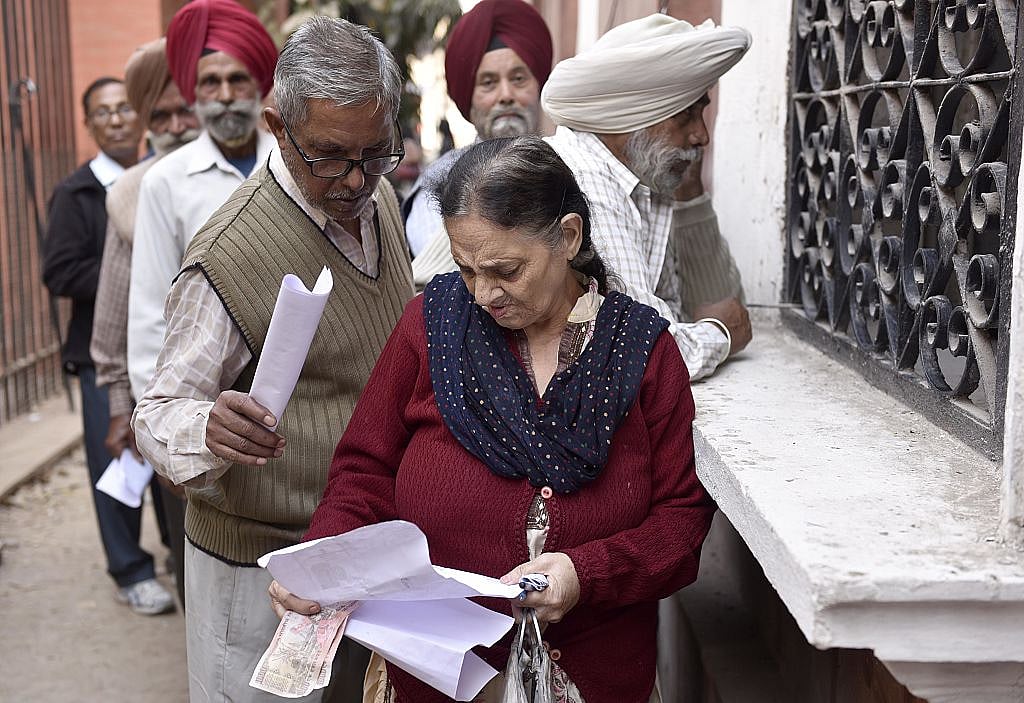

PMO goofs up on senior citizens too

What the Prime Minister held out as a ‘sop’ for senior citizens turns out to be a reduction on existing benefits! Both Finance Ministry and the PMO seem to have got their numbers wrong

In his address to the nation on New Year’s Eve, Prime Minister Narendra Modi was not only made to announce old schemes as ‘new’ but the PMO, which would have vetted his speech and provided inputs, also made him mouth sops for senior citizens which actually are not sops but reduce existing benefits.

The Prime Minister seemed to suggest in his address that senior citizens would get an assured interest of 8% on deposits up to ₹7.5 lakhs locked in or fixed for 10 years.

Instead of placating the senior citizens, this appears to have incensed them because what the PM said amounted to an infringement on the existing scheme.

Senior Citizen Saving Scheme in Post Offices and SBI allows people above 60 years of age to deposit ₹15 lakhs for 5 year-lock-in period to earn interest @ 8.6% per annum ( It used to be 9% earlier) with interest payable quarterly which earns them roughly ₹10,000 a month.

The PM has just reduced the ceiling of deposit to half to ₹7.5 lakhs and also the interest to 8% and presented it as a progressive step for the benefit of senior citizens.

Senior Citizen Saving Scheme in Post Offices and SBI allows people above 60 years of age to deposit ₹15 lakhs for 5 year-lock-in period to earn interest @ 8.6% per annum, which earns them roughly ₹10,000 a month.The PM has just reduced the ceiling of deposit to half to ₹7.5 lakhs and also the interest to 8% and presented it as a progressive step for the benefit of senior citizens

Politically the Government or the ruling party may not be concerned with the constituency as a vote bank because only 8.6% of the population or 10.38 crore people were above the age of 60 in the 2011 Census compared to 7.66 crore (5.6%) in 2001.71% of the elderly are said to be residing in villages. But their number is growing and a welfare state which is unable to provide them with medicare and other old-age benefits may well attract criticism for reducing interest payment on their own savings.

An irate senior citizen hoped that though the PM is a “smart salesman” who can sell combs to the bald, he would not get away by taking senior citizens for a ride.

Another irate senior citizen said, “It is worth recalling that as on 1.1.2016, the Senior Citizens Savings Scheme (SCSS) the interest rate was 9.3% and a senior citizen together with his spouse could deposit a maximum of ₹15 lakhs and had to block it for 6 years.”

“Even now the interest rate is a bit above 8% and quite possibly will now be brought down to less than 8%. There is a determined effort to bring down the rate of interest on deposits but one thought the senior citizens would be spared since bulk of them depend on their interest income only.”

“Even now the interest rate is a bit above 8% and quite possibly will now be brought down to less than 8%. There is a determined effort to bring down the rate of interest on deposits but one thought the senior citizens would be spared since bulk of them depend on their interest income only. Now that banks are flush with funds, what is the justification for reducing the interest rate on the Senior Citizens Savings Scheme?”

“The justification given was that with high interest rates on such schemes, the Banks were finding it difficult to mobilise funds. Dubious as the proposition was, now that banks are flush with funds, what is the justification for reducing the interest rate on SCSS ?” he asked.

Yet another senior citizen, a former bureaucrat, told National Herald, “ A lowering of inflation does not mean that prices are going down. It only means that things are becoming dearer at a slower rate. Therefore a lower rate of Inflation alone cannot justify a lower interest rate and reduction of income of those who live on the monthly interest they get on their savings.”

Senior citizens , a majority of whom enjoy neither pension nor the benefits of PF, also wonder why the interest rate allowed on the Public Provident Fund is lower than PF.

Join our official telegram channel (@nationalherald) and stay updated with the latest headlines