How to Manage Critical Illness & Death Risks with the Right Insurance Plans

Healthcare costs are rising. Whether it's hospitalisation, surgery or follow-up care, having a health insurance policy ensures your savings remain untouched while you focus on recovery

You work hard to build a secure future, so why not protect it? As medical bills climb and life throws surprises, health and term insurance step in to offer peace of mind.

Whether it's handling hospital expenses or supporting your loved ones in your absence, the right cover makes all the difference.

Why is Health Insurance a Must-Have?

Healthcare costs are rising across India, especially for long-term and critical illnesses. Whether it's hospitalisation, surgery, or follow-up care, having a health insurance policy ensures your savings remain untouched while you focus on recovery.

What Counts as a Critical Illness?

Critical illnesses are serious medical conditions that usually need long-term treatment and higher expenses. These include:

Heart attack or bypass surgery

Cancer (all types)

Stroke

Kidney failure

Major organ transplant

Permanent paralysis

Multiple sclerosis

These conditions may interrupt income or require specialised care, both of which can strain your finances.

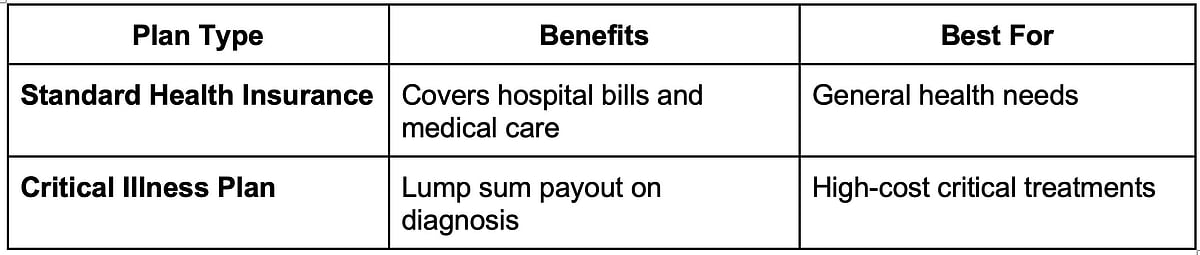

Two Insurance Options to Manage Critical Illness

Two types of plans can help you deal with these health challenges:

1. Comprehensive health insurance plans

These cover hospital expenses and often include the following:

● In-patient hospitalisation

● Daycare procedures

● Pre- and post-hospital care

● Ambulance and ICU charges

● Cashless treatment at network hospitals

2. Critical illness-specific plans

These pay a lump sum amount upon diagnosis of a listed illness, regardless of treatment cost. You can use the payout to:

● Cover medical bills

● Manage day-to-day expenses

● Opt for better treatment or second opinions

Why Health Insurance Is the First Line of Defence?

Access to quality healthcare without delay

Helps protect your long-term savings

Reduces the burden on family members

Cashless options ease the treatment process

Securing Your Family's Future with Term Insurance

It's not just about you—it's about your family. A sudden absence can disrupt their entire lifestyle. That's where term insurance comes in. It offers a simple and cost-effective way to secure your loved ones financially, even when you're not around.

What is Term Insurance and Why Does it Matter?

Term insurance is a life cover that pays a fixed sum to your nominee if something unfortunate happens to you during the policy term. It's affordable, flexible, and designed for long-term peace of mind.

Key Advantages of Term Insurance

Term insurance has many benefits that make it one of the most reliable financial safety nets for families.

1. High cover at a low premium

Especially if you buy early

2. Customised payout options

Lump sum, monthly income, or both

3. Riders for extra protection

Add-ons for critical illness, accidental death, and more

4. Tax savings

Offers tax advantages under Sections 80C and Section 10(10D) of the Income Tax Act

How Does it Support Your Family's Goals?

If anything unexpected occurs, your term insurance policy will ensure your family can:

Maintain their regular lifestyle

Pay for school or college fees

Clear home loans or EMIs

Cover daily needs and medical costs

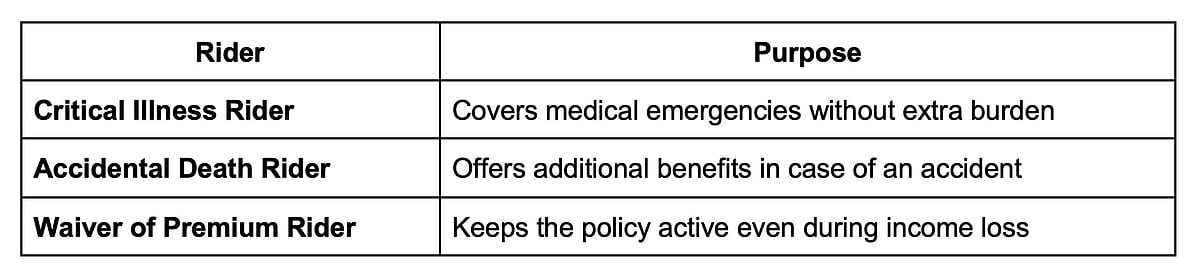

Add-On Riders That Strengthen Your Coverage

Enhance your insurance policy with powerful add-on riders that offer extra protection when life takes an unexpected turn.

1. Critical Illness Rider

Helps you financially if you are diagnosed with a major illness

2. Accidental Death Rider

Gives your family additional support in case of an accident

3. Waiver of Premium Rider

Future premiums are waived if the policyholder is disabled

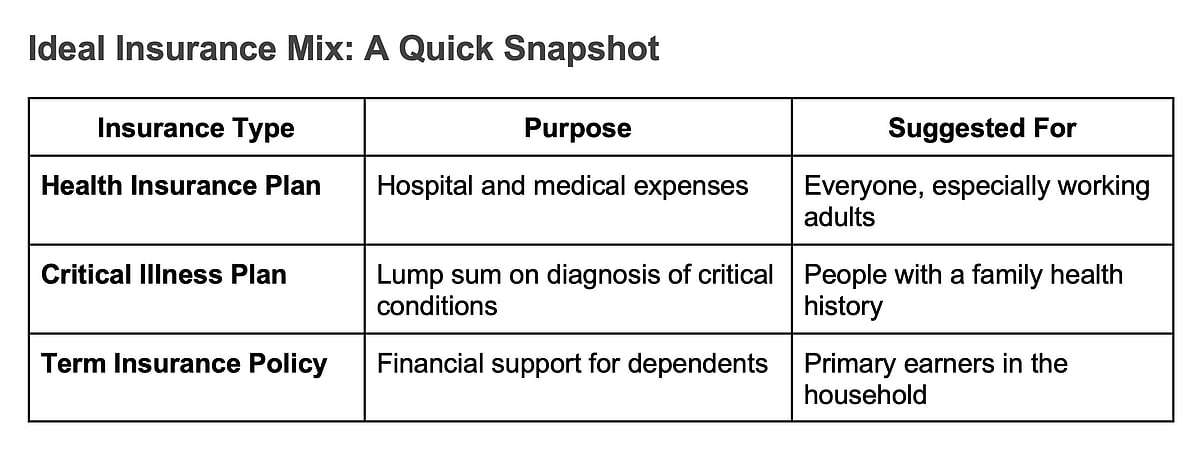

Combining Health and Term Insurance for Full Protection

While health insurance focuses on your medical needs, term insurance covers your family's future. Together, they offer complete risk protection for your health and household finances.

How to Choose the Right Plans for You?

Not every plan fits everyone. Here's how to find one that works for your unique needs:

1. Understand your life stage

Single, married, or with dependents

2. Evaluate financial responsibilities

Loans, education costs, dependents

3. Start early

Younger buyers pay lower premiums for the same cover

4. Check insurer reputation

Go for companies with good claim settlement ratios

5. Add useful riders

Especially if you have a family history of illness or a risky job

6. Review annually

Update your policy based on life events like marriage or parenthood

You work hard to provide the best life for your family. Insurance helps you protect that effort.

Choosing both health insurance and term insurance is a smart way to ensure that no matter what life brings, your loved ones are never left vulnerable.

Join our official telegram channel (@nationalherald) and stay updated with the latest headlines