Is One Life Insurance Policy Enough for All Your Financial Goals?

A policy designed for family protection may not create the exact payout pattern needed for a child’s college fee

A single life insurance policy can be a strong beginning. It can give the family protection, create discipline and bring a sense of order to financial planning. But whether one policy is enough for all financial goals depends on how large and varied those goals are. A person with no dependants and limited liabilities may need a simpler structure. A person with children, a home loan, ageing parents and retirement goals may need a more layered approach.

To understand this properly, return to the life insurance meaning in practical terms. A life insurance policy is meant to provide financial support according to the policy terms when a specified event occurs, usually the death of the insured person, or maturity in the case of certain plans. Different policies can serve different roles: protection, savings, income, retirement planning or legacy support.

One policy can work when the goal is narrow

If your primary need is income protection for dependants, one adequately sized term-oriented policy may cover that role. If your goal is a specific future expense, one savings-oriented policy with a suitable maturity date may also be enough for that goal. The trouble starts when one policy is expected to act like every tool in the financial drawer.

A policy designed for family protection may not create the exact payout pattern needed for a child’s college fees. A plan chosen for guaranteed income may not be the right size for a large home loan protection need. A retirement-focused plan may not solve short-term liquidity needs. This does not make any of these policies less useful. It means each one should be given the right job.

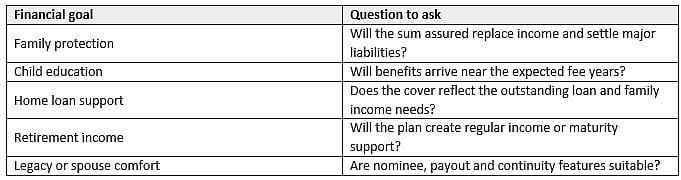

Map goals before counting policies

This mapping exercise is useful because it prevents random policy accumulation. The answer may be one policy, two policies or more, but the decision should come from goal structure, not anxiety or sales pressure.

Why layering often makes sense

Layering means using different policies or financial products for different purposes. A young family may keep one high-cover protection policy, one savings plan for a child’s future, and later add a pension or annuity-oriented plan for retirement. This creates cleaner planning. The family knows which policy serves which goal.

· Protection layer: supports dependants and liabilities.

· Savings layer: builds benefits for planned milestones.

· Income layer: helps with future regular cash flow.

· Legacy layer: supports spouse or nominee-related goals.

The benefit of layering is clarity. When every policy has a named purpose, reviews become easier. You can increase cover when responsibilities rise, continue goal-linked plans for their intended maturity, and add retirement income planning when the time is right.

When one policy may become insufficient

Life changes gradually and then suddenly. A policy bought before marriage may not reflect the needs of a spouse and child. A policy bought before a home loan may not account for the loan. A policy bought when income was lower may not match the family’s current lifestyle. This is why adequacy should be reviewed after major life events.

1. Marriage or addition of a dependant

2. Birth or adoption of a child

3. Taking a home loan or major business loan

4. Sharp increase in income and lifestyle expenses

5. Planning for children’s higher education

6. Beginning serious retirement planning

These events do not automatically mean you must buy another policy. They mean the existing cover and benefits should be checked. Sometimes increasing cover or adding a suitable rider may help. Sometimes a separate policy for a separate goal is cleaner.

Avoid mixing every expectation into one plan

A common mistake in financial planning is wanting one product to provide high cover, high savings, liquidity, guaranteed income, tax efficiency, low premium and retirement support all at once. Real financial planning is usually more modest and better organised. Each feature has a cost, a condition and a purpose. When expectations are separated, the decision becomes more mature.

A life insurance policy should be read for what it promises clearly. What is the death benefit? What is the maturity benefit, if any? What are the premiums? What happens if premiums stop? What is the claim process? Once these are understood, it becomes easier to decide whether the policy can carry one goal or several.

Reviewing policies is part of owning them

Policy ownership should not end after paying the first premium. Review the plan every few years. Check nominee details, contact information, premium mode, coverage amount, policy term and goal relevance. Keep documents accessible to the family. If there are multiple policies, maintain a simple summary sheet with policy number, insurer, premium due date, nominee and purpose.

This small habit can make life insurance more useful. It turns policies from forgotten paperwork into an active part of the household’s financial structure.

The practical answer

One life insurance policy may be enough if your financial goals are limited, your cover is adequate and the policy’s benefits match the intended need. But as life becomes more layered, insurance planning may also need layers. Protection, savings and retirement income do not always fit neatly inside one policy.

The better approach is to begin with your goals, assign each goal a time frame and then see whether the existing policy can honestly serve them. If it can, keep it reviewed. If it cannot, adding another suitable life insurance policy may bring more order to the plan. The point is not to own many policies. The point is to make sure every important financial goal has a dependable structure behind it.

This is an advertorial. The article is published as received.

Join our official telegram channel (@nationalherald) and stay updated with the latest headlines