Should You Increase IDV during Renewal?

A car loses value as it gets older due to depreciation, usage and general wear

Renewal is the right time to check whether your car’s insured value still matches its current market value. IDV, or insured declared value, matters most if the vehicle is stolen or declared a total loss.

Increasing it may offer wider financial comfort, but it can also affect the premium. So, the decision should depend on your car’s age, condition, usage, resale value and renewal cost.

How IDV Works in Car Insurance

In car insurance, IDV is the maximum amount the insurer may pay if the vehicle is stolen or damaged beyond repair, subject to policy terms. It is linked to the vehicle’s market value and is usually fixed at the start of the policy period.

A higher IDV can increase the own damage premium because the insurer takes a higher risk. A lower IDV may reduce the premium, but it can also reduce the claim amount in total loss or theft cases. So, the aim should be balance, not simply choosing the highest or lowest number.

Why IDV Changes at Renewal

A car loses value as it gets older due to depreciation, usage and general wear. This is why the IDV usually reduces at every renewal. The insurer may suggest an IDV based on the vehicle’s age, model, variant, location and other relevant factors.

However, the suggested figure may not always match what you feel is suitable. You can review it before renewal and check whether it is close to the car’s realistic market value. The final IDV should be reasonable and acceptable as per the insurer’s rules.

Should You Increase IDV?

You may consider increasing IDV if the suggested amount looks much lower than the current market value of the car. This may be relevant when the car is relatively new, well-maintained or has a strong resale value.

Regardless, increasing IDV only to get a higher possible claim amount may not always be practical. It can raise the premium, and the insurer may still approve only a reasonable IDV based on the vehicle details. The increase should make sense for the car’s age and condition.

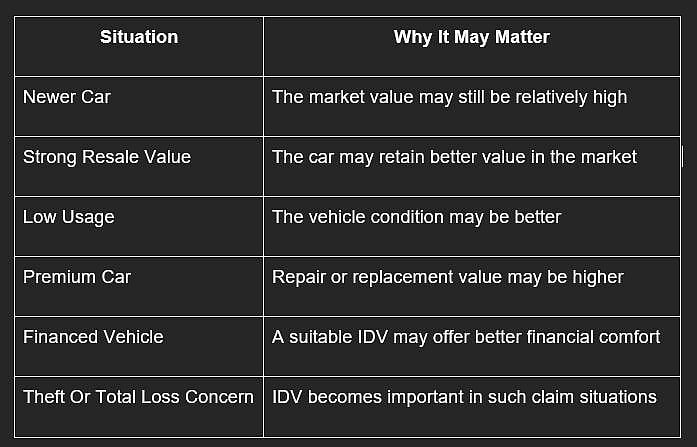

When a Higher IDV May Be Useful

A higher IDV may be worth reviewing when the car’s current market value is higher than the suggested renewal value. This can be relevant in the following cases:

This does not mean increasing IDV is necessary for every car owner. It simply means you should check whether the suggested IDV is close to your car’s current market value before renewing the policy.

When Increasing IDV May Not Be Needed

Increasing IDV may not be useful if the car is very old, rarely used or has a low market value. In such cases, paying a higher premium for a higher declared value may not feel practical.

It may also be unnecessary if the suggested IDV is already close to the vehicle’s market value. A very high IDV that does not match the car’s age and condition may not be accepted during policy issuance. Also, if you only have third party car insurance, IDV is not a key factor because this cover does not pay for damage to your own car.

Check Premium Impact before Deciding

Before increasing IDV, check how much the premium changes. A higher IDV may increase the own damage premium, so the extra cost should be reasonable compared to the added protection.

Also check deductibles, add-ons, no-claim bonus and claim terms. These factors can affect the overall value of the policy. The right IDV should support your financial comfort without making the renewal cost unnecessarily high.

How to Choose a Suitable IDV

Follow a simple approach during renewal:

● Check the insurer’s suggested IDV

● Compare it with the current market value

● Consider the car’s age and condition

● Review usage and location risks

● Check the premium difference

● Avoid choosing an unrealistically low value

● Avoid increasing IDV without a clear reason

● Read the policy terms before payment

This helps you make a practical choice instead of selecting IDV only to reduce or increase the premium.

Final Thoughts

Increase IDV during renewal only if the suggested value seems lower than your car’s realistic market value. A suitable IDV can help in theft or total loss cases, but it may also affect the premium.

The right approach is to keep it balanced. Check the car’s age, condition, usage, resale value and renewal cost before deciding. If the current IDV is fair, increasing it may not be necessary.

Join our official telegram channel (@nationalherald) and stay updated with the latest headlines