Are alleged inefficiencies in PSU Banks due to interference by Government?

While the Government is determined to privatise PSU banks on grounds of inefficiency, they support the credit needs of a population not quite in the field of vision of private banks

Privatise all public sector banks (PSBs) except State Bank of India, suggested a research paper written jointly by NCAER (National Council of Applied Economic Research) director general Poonam Gupta and former vice-chairman of NITI Aayog, Arvind Panagariya in August. Do not privatise all PSBs in one go, argued another paper published in the RBI Bulletin, which supported a ‘gradual approach’.

It’s not without any basis that privatisation has become a lazy byword for ‘efficiency’. Nor is it hard to understand why public sector undertakings are equated with a lack of said efficiency. But it’s not as straightforward as it may seem in drawing room conversations. In the case of public sector banks, the conundrum is possibly even more intricate.

Poonam Gupta and Arvind Panagariya argue that PSBs have the potential to distort credit flow for political gain, undermine private banks and bleed the public exchequer through periodic bailouts of PSBs. They see no redeeming features in public sector banks. On the other hand, the paper in the RBI Bulletin concludes that while private banks (PVBs) may be more profitable—and, by that measure, more ‘efficient’—PSBs are more inclusive and still have a big role to play in the Indian economy. Remarkably, after a hue and cry in the media—with analysts erroneously concluding that the RBI paper was opposing privatisation—the central bank went on the defensive with the disclaimer that the opinion expressed in the paper was the researchers’ own and did not reflect the views of the RBI.

In fact, the RBI paper was only advocating a graduated, soft-landing approach to privatisation of public sector banks, but that subtlety was lost in the headlines. In effect, it said: not all PSBs at one go, privatise two PSBs to start with.

The intent to privatise PSU banks was made known in 2020. In the Union budget for 2021-22, finance minister Nirmala Sitharaman announced that the government would disinvest out of two PSU banks, without naming them. In June, there were reports that NITI Aayog had shortlisted four smaller PSU banks for privatisation. On 18 July, Sitharaman reiterated the government’s commitment to privatise state-owned banks, but there has been no action since.

There are 12 PSBs in which the government has a controlling stake. These are: State Bank of India (SBI), Punjab National Bank (PNB), Canara Bank, Bank of Baroda, Bank of India, Punjab and Sindh Bank, Indian Overseas Bank, Bank of Maharashtra, UCO Bank, Central Bank of India, Union Bank of India and Indian Bank (after its merger with Allahabad Bank).

The four banks shortlisted—but officially undisclosed—by Niti Aayog, were identified in the media as IOB, Bank of Maharashtra, Bank of India and Central Bank of India. Bank of India has a workforce of about 50,000 and Central Bank of India has 33,000; Indian Overseas Bank employs 26,000 and Bank of Maharashtra about 13,000, according to estimates by bank unions.

The lower profits of public sector banks, higher administrative expenses, higher manpower and mounting NPAs (non-performing assets) are reasons frequently cited to privatise them. On top of it, there is growing adherence to the belief that the ‘government has no business being in business’.

Being government-owned, PSBs are forced, it is pointed out, to deploy capital, manpower and time to programmes such as Hindi Pakhwada, Vigilance Pakhwada and Swachh Bharat Pakhwada, which these banks have no (business) reason to be associated with. True enough.

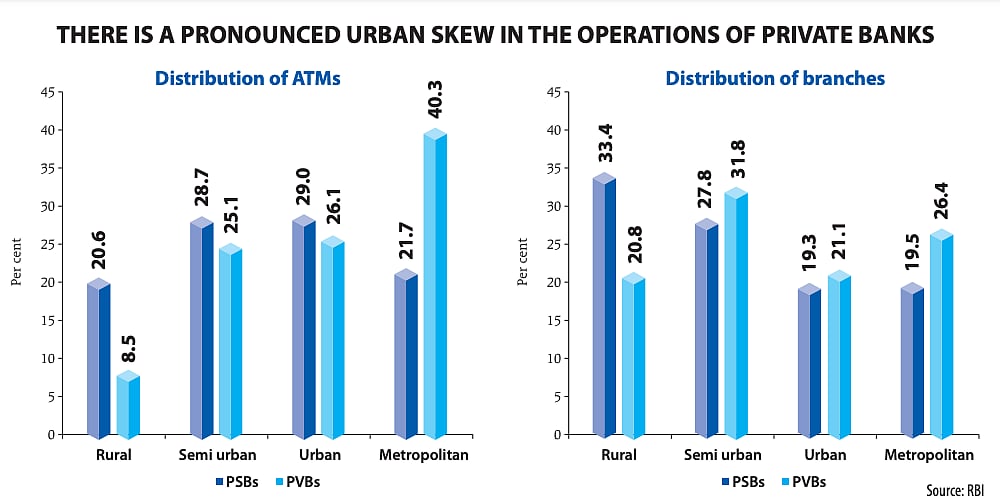

There is admittedly a lot to support the conviction that the government should get out. What is usually left unsaid is that a dilution of stake (simply to raise money) is not the same as pulling out fully, and in a way that the government cedes control. What is also left unaddressed or under-addressed in this line of argument is how to support the credit needs of uncorporatised small businesses, which still account for most of the jobs in the country, or the rural sector, which is by far larger than the urban sector that private banks tend to focus on. (see graphics)

Economist M. Govinda Rao, a member of the 14th Finance Commission and currently chief economist, Brickworks Ratings, underlines the part PSBs play in financing small and medium industries. “While the private sector has increased its lending to the SME sector, there is a sound reason why the government needs to retain the public sector banks. The fact that SMEs will play a vital role in shaping the country’s economy and the government has an agenda to carry out in the social space make PSBs important to be. To Attain its goals, the government should retain the public sector banks because it makes a significant difference to the lending pattern when it comes to the SME sector in India,” he says.

The rural branches of PSBs contribute little to their profits. Will they continue to be in focus when PSBs are privatised, and the profit motive starts dictating business decisions? If not, will it mean a return to days prior to their nationalisation, back in 1969 and again in 1980? (14 banks were nationalised in 1969 while another six were nationalised in April 1980). How will the ‘profit-first’ motive of private banks impact the national commitment to social welfare, inclusive credit and ‘priority sector’ lending?

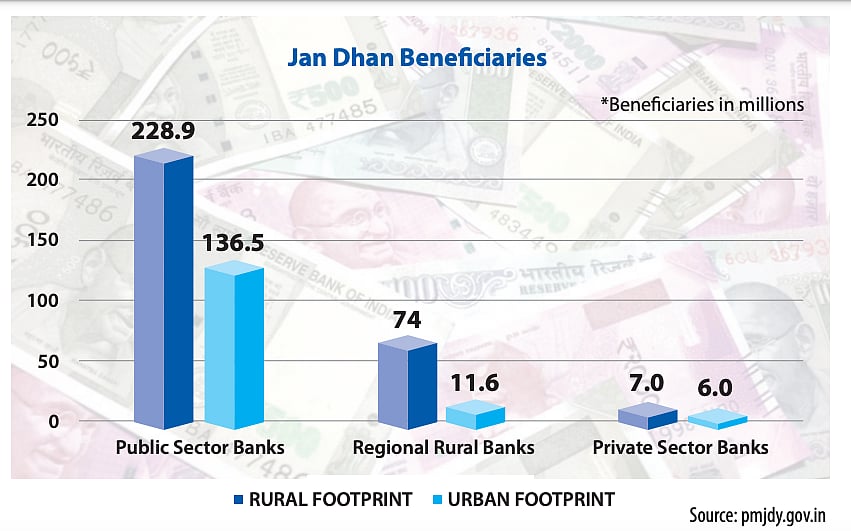

If private banks were to handle schemes like the zero-balance Pradhan Mantri Jan Dhan Yojana or the Suraksha Bima Yojana, will they undertake their disbursal at minimal cost? What about charges and fees levied on issue of passbooks and cheque books, on ATM cards, on cash withdrawals and other services? Will they not go up and become higher and barely affordable for people who make do with meagre incomes?

And what about the million-plus employees in public sector banks? Won’t private sector ‘efficiency’ have a bearing on their future? Madan Sabnavis, chief economist at Bank of Baroda says: “When three public sector banks merged, nobody lost jobs. When a private player takes over, job cuts are inevitable. Look at Air India, where a VRS is under way."

Even apart from the humanitarian aspect of this riddle, there is a noteworthy ‘efficiency’ dimension to it: from the perspective of labour cost efficiency, the analysis by RBI researchers shows that PSBs have, in fact, done better than private banks on that score—in other words, if PSBs have incurred higher costs on labour, they have also generated higher output per unit of labour.

Sabnavis argues that even on financial efficiency parameters, the gap is narrowing between PSBs and private banks. “Public sector banks are better placed today because they have cleaned up their NPAs,” he says.

The other real question, he says, is: how critical is it for the economy that the government run these banks? “Only the government can answer [that] question. The Jan Dhan accounts [for example] are a high-cost account as far as banks are concerned; private banks are nowhere in the picture,” he says, suggesting that priority lending will take a hit if PSBs are not in the picture.

Even the RBI paper underlines the pivotal role of public sector banks in infrastructure finance, so critical to largescale development activity.

Gupta and Panagariya maintain that the banks chosen for privatisation must be the ones with the highest returns on assets and equity, and the lowest NPAs in the past five years. Economist Ajay Abhyankar finds this absurd. “Banks offering the highest returns on assets and equity and with the lowest NPAs are the best among PSBs. If you sell the best and most profitable [public sector] banks, when they are supporting jobs and rural economies, the motives must be suspect,” he says.

Abhyankar urges us to remember: “During the global financial crisis of 2008, India survived because of public sector banks and insurance companies. They weren’t carried away by the speculative frenzy of the international market. PSBs ensure financial stability and sanity.”

It may be germane to the debate, then, to ask if the problem with public sector banks is their efficiency per se or the government’s longarm methods of exercising control on their operations, which impair their efficiency.

Join our official telegram channel (@nationalherald) and stay updated with the latest headlines