GST: Centre-State relations do not depend on legality alone

Taking GST dispute to SC is unlikely to work but states are justifiably upset because they get no share from the Centre’s cesses and surcharges on items like petrol, diesel, education, health, etc.

On the issue of denying the payment of GST compensation to the States and instead asking them to borrow, the Centre may have been legally correct, but it must not be forgotten that the states, irrespective of the colour of the ruling dispensation, had made a huge sacrifice of their autonomy in surrendering their taxing powers while agreeing to implement the GST regime to usher in a unified market throughout India based on what was promised to be a “Good and Simple Tax”. The promise remains to be fulfilled yet.

Multiple rates, technical glitches in the backbone IT-architecture of GSTN and difficulties faced by the taxpayers on various counts that have bedevilled it since launch still remain unaddressed even 3 years later. The latest decision of the GST council may have made the waters a little murkier, driving a wedge between the Centre and the States which have so far wonderfully cooperated in the GST Council that has, barring a single occasion, voted unanimously on all contentious issues.

This is not to undermine the positive benefits the GST has already brought. It was supposed to be a transformational tax, and in many ways it has been so. It not only eliminated 17 different taxes and 13 cesses which were earlier levied by the Centre and the States, it has brought down the rate of effective tax and its incidence on most items. The ominous Inspector Raj and long queues of trucks at the state entry barriers are things of the past. Even in a country with a highly fractious political culture, the GST Council has set a shining example of cooperative federalism. However, the future may not be as smooth.

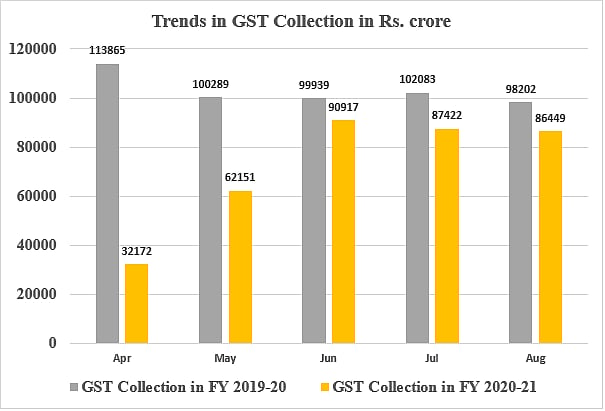

Even before the pandemic had struck, GST revenues were falling. Now the pandemic has wrought havoc in the collections which are nowhere near the last year’s level. As per the GST Compensation Act, the Centre is supposed to pay compensation to the states, payable bimonthly for 5 years till FY22, in case the revenue loss of the states exceeded 14 percent growth calculated on the base-year 2015-16 collections, from the GST Compensation Fund built up by the Compensation Cess levied on luxury and sin goods like cars, tobacco products and soft drinks.

GST payments to states for the current fiscal have been pending since April 2020. The total compensation released for 2019-20 was about Rs 1.65 lakh crore, as against compensation fund collections of just Rs 95,444 crore, and the Centre had to tap the balance of cess from the previous years as well as Rs 33,412 crore from the Consolidated Fund of India on account of IGST to meet the States’ dues. Thus the inability to pay states’ GST dues was not just due to the economic situation triggered by the pandemic. On the average, the actual collections under the fund are only about half of the average monthly requirement of Rs 14,000 crore.

The reduction in GST rates for many items had resulted in an inverted duty structure where the duty on the final product was less than the duty on the inputs, requiring higher refunds.

The options before the GST Council were either to (1) rework the slabs or increase rates to correct the inverted duty structure; (2) increase the rates of compensation cess and expand the item base, or (3) allow the states to borrow more and repay the borrowing using future collections, that is, by extending the compensation cess beyond 2021-22.

Given the mayhem caused by the pandemic and the severe contraction of the GDP driving the economy into a comatose state, the Centre was wary of raising or expanding the scope of the cess that might cause further job-losses. It was suggested that the GST council could also borrow, but it has no such mandate, being a Constitutional body. Centre thus had only two options before it: either allow the states to borrow or meet the shortfall from its own resources which must come from its own borrowings, which would have its fiscal and monetary implications.

For one thing, yields of government securities (G-Secs) will harden, putting pressure on interest rates across the economy. This might also be viewed negatively by the credit rating agencies. Besides, with the fiscal deficit already having exceeded the full year target of Rs 7.96 lakh crore by more than 3 percent in July, it was really a Hobson’s choice for the Centre.

The Act does not deal with any shortfall of compensation cess which never happened before, and the reason partly is the inefficiency of the GSTN to fix the technical glitches, especially those related to the automated matching of buyers’ and suppliers’ invoices. The Centre had earlier approached the Attorney General who opined that it was not legally obliged to pay the full compensation. Armed with such opinion, in the GST Council meeting of August, it offered the states two options, the logic of which is questionable.

It has cited the unprecedented economic contraction and consequent revenue shortfall due to the pandemic as an “Act of God”, which is not covered by the GST statute that has no force majeure clause, to renege on its promise to pay the States compensation out of its own funds.

As it had held, “Parliament obviously could not have contemplated a historically unprecedented situation of huge losses of revenue from the base—arising from an Act of God quite independently of GST implementation—affecting both Central and State revenues, direct and indirect”, and that “This is a national problem not a Central Government problem alone.” There is also no denying that due to the Chinese action on the LAC, higher Central expenditure was necessitated also by the needs of national security.

The estimated compensation shortfall to the states in the current fiscal is Rs 2.35 lakh crore. The Centre did some accounting jugglery to divide this into two segments, shortfall of Rs 97,000 crore on account of GST implementation and the rest attributable to the Covid-19 pandemic that has caused a revenue loss.

Accordingly, it offered two options to the states: Option-I for additional borrowing of Rs 97000 crore under a special borrowing window of the RBI at G-Sec-linked interest rates, to be repaid in full including interest from the compensation cess fund, without being counted as States’ debt, while the rest Rs 1.38 lakh crore will be reckoned as state debt.

Option-II was allowing them to borrow the entire amount of Rs 2.35 lakh crore from the market, of which only the principal will be paid from the compensation cess while the interest burden will lie on the States’ shoulders; however, it now appears that the Centre might allow the interest also to be paid from the cess without creating any burden on the exchequer. The compensation cess will continue to be levied beyond FY22 till the States’ debts get liquidated.

Earlier in May, under the Centre’s Covid-19 stimulus package, States were given additional borrowing space by raising their borrowing limits from 3 to 5 per cent of GSDP, but save only 0.5 percent which was unconditional, the rest was available only on their implementation of various reform measures like One Nation One Ration Card, Ease of Doing Business, power distribution, and augmentation of municipality revenues.

Even the “unconditional” 0.5 percent was actually conditional upon achievement of the milestones prescribed in respect of the above. Now Option-I allowed the States to carry forward any unutilised borrowing space up to 1 per cent of GSDP unconditionally to the next fiscal. The Centre would coordinate the borrowing and also bear the extra interest cost above the G-Sec yield through a subsidy. However, no such extra borrowing space would be available for Option-II; the entire borrowing exceeding Rs 97000 crore will count as the States’ liability. Neither would the cost of borrowing be linked to G-Sec yields but would be decided by the market.

States which were demanding that the borrowing instead be done by the Centre are understandably furious at what they see as “betrayal”, especially the non-BJP ruled ones like Punjab, Delhi, Puducherry, Kerala, Madhya Pradesh, Rajasthan and Chhattisgarh. They feel the distinction in the shortfall on account of GST implementation and the pandemic is “unconstitutional”. In any case, they want the entire borrowing to be accommodated by increasing the borrowing limit. They are apprehensive that the borrowing would translate into “mortgaging of the future”.

Kerala has earlier threatened to take the matter to the Supreme Court which remains an option, but given the nature of the dispute, may not find much traction there. States have a legitimate grouse not only because the delay in compensation payment has pushed their already precarious finances to the brink, putting serious constraints upon their ability to deal with the unprecedented crisis. They are also angry because they get no share from the various cesses and surcharges levied by the Centre on sundry items including petrol, diesel, education, health, social welfare etc.

Understandably it was not an easy decision for the Centre, but it goes against the spirit of co-operative federalism so far demonstrated convincingly by the GST Council. Instead of insisting on legalities, the Centre could have persuaded the states to come on board as on the earlier occasions.

As regards the ability of the States to raise loans from the market, there may not be much difficulty. The market is awash with liquidity due to the liquidity-dominant stimulus package with little demand for credit, as evidenced by the FCI being able to raise loans of Rs 75000 crore at only 4.6 percent. Banks are flush with funds which are being parked at the RBI at the reverse repo rate. But the Centre still has time to strike a bargain with the States – especially for increasing their borrowing limits to accommodate the entire Rs 2.35 lakh crore. Healthy federal relations rarely depend on legality alone.

(The author is former Director General, Office of the Comptroller & Auditor General of India. Views are personal)

Join our official telegram channel (@nationalherald) and stay updated with the latest headlines