Adani looks at confidence-building measures as group prepays $1.1 billion

Prepayment in light of recent market volatility and promoters’ commitment to reducing overall leverage; Adani Enterprises share price has 40 per cent more downside, says NYU professor

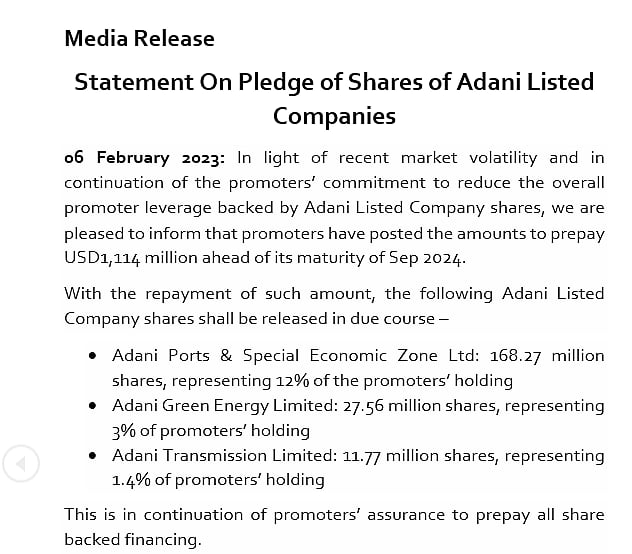

The promoters of Adani Group firms have prepaid $1.1 billion, or approximately Rs 9,000 crore, in debt ahead of its due date in September 2024.

The conglomerate made the payments, according to a statement from the business house, "because of recent market volatility and in continuation of the promoters' commitment to limit overall promoter leverage supported by Adani listed company shares."

Approximately 16.8 billion shares in Adani Ports & Special Economic Zone Ltd. (12% of founders' stock), 2.75 billion shares in Adani Green Energy Ltd. (3 per cent), and 1.17 billion shares in Adani Transmission will be released as a result of this prepayment (1.4 per cent).

The prepayment action comes after Hindenburg Research accused Adani Group of employing shady offshore tax havens and manipulating stock prices. Following recent market volatility and a pledge to minimise overall promoter leverage backed by listed business shares, the firm said that promoters have deposited the sums to prepay $1.11 billion ahead of their maturity of September 2024. Adani Green Energy, Adani Ports, and Adani Transmission are the three companies.

Shares of three publicly traded firms would be released in due course with the payback of such a sum. The businesses include the 168.27 million shares of Adani Ports & Special Economic Zone, which account for 12 per cent of the promoters' ownership. Adani Transmission's promoter holding of 1.4 per cent and Adani Green Energy's promoter holding of approximately 3 per cent will both be published.

Adani Enterprises was valued at Rs 945 per share in an interview with CNBC TV18 by Professor Aswath Damodaran of New York University's Stern School of Business. According to Damodaran, his value was made with a very liberal margin and included a revenue estimate given the current turbulence the group is experiencing in the wake of the publication of the Hindenburg Research report.

“Adani Enterprises typically invests in infrastructure industries, which have a long gestation time and are unlikely to produce substantial returns,” according to Professor Damodaran. 4.8% to 5% is the average annual return for infrastructure enterprises worldwide. He stated in the interview that "the additional capital that the Adani Firm has raised has been virtually completely debt-based, meaning the group is reliant on debt for expansion."

Professor Damodaran expressed worry that something might be pushing stock prices higher without a competing force on the other side. Additionally, he believes that while determining which Adani Group companies to include in indices, the MSCI should take market size into account.

Meanwhile, Standard Chartered, has reportedly stopped accepting Adani Group bonds as a security for margin loans, according to BT. This comes following announcements of comparable actions by Citigroup and Credit Suisse, both of which ceased lending on dollar bonds issued by the Adani Group.

According to a story by the Economic Times, certain StanChart relationship managers reportedly warned their private wealth clients in Asia's major markets, including Singapore, that the bank would not accept these bonds as security. As per the article, the decision was made on Friday and is only temporary.

Join our official telegram channel (@nationalherald) and stay updated with the latest headlines