Banks let down by RBI and BJP’s ‘politics’

These are the same banks which had passed the litmus test during the global financial crisis in 2008. Then why have our banks all of a sudden started looking like institutions on shifting sand

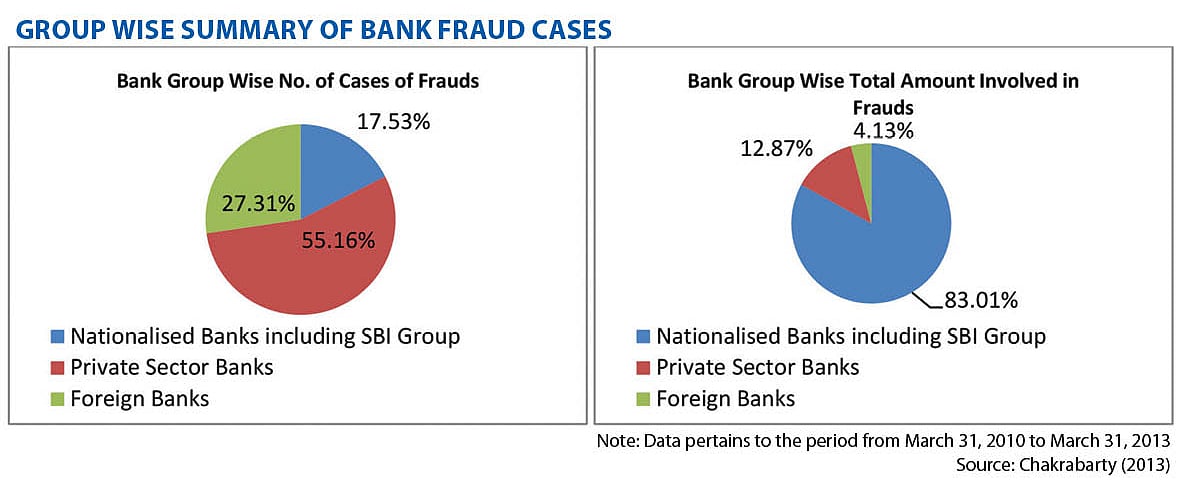

The entire banking sector in the country is in the news for all the wrong reasons. The latest has been the arrest of the sitting and former Chairmen and Managing Directors of a Pune-based state-run lender, Bank of Maharashtra. It was preceded by the MD & CEO of the country’s largest private sector bank ICICI Chanda Kochhar being asked to proceed on leave until the completion of an investigation into charges of abusing her office to benefit her husband and family.

There have been quite a few other arrests involving bankers in recent months. The former Punjab National Bank MD & CEO, Usha Ananthasubramanian, was first transferred to a much smaller state-owned lender, Allahabad Bank and then was divested of her powers following the much talked about ₹13,000 crore bank fraud allegedly orchestrated by fugitive jeweller, Nirav Modi.

Former IDBI Bank CMD, Yogesh Agarwal was also arrested along with other senior officials of the bank in the Vijay Mallya loan default case a year ago. Bank of Baroda’s executive director, KV Rama Moorthy, was shunted to a much smaller lender, United Bank of India after his name figured in a fraud which took place in Dubai. In yet another case, the CMDs of Indian Bank and IDBI were swapped. MK Jain, who has the credit of turning around Indian Bank he was heading in the past, was rewarded by the government when he was asked to head a bigger but debt-laden bank, IDBI. Recently Jain was elevated to the post of RBI’s deputy governor.

The issue is what has gone wrong with the banking system of the country? These are the same banks which had passed the litmus test during the global financial crisis triggered in 2008 by the collapse of Lehman Brothers. Then why have our banks all of a sudden started looking like institutions on shifting sand or a castle of cards?

See our banks being laden with a pile of NPAs, amounting to ₹10 trillion. To understand the issue well, one needs to take a deep dive into the affairs of the banking sector during the past few years.

Bank staff demoralised in aftermath of demonetisation

It all started with the mega launch of Pradhan Mantri Jan Dhan Yojana in the very year Prime Minister Narendra Modi assumed his office. All the state-owned banks were given huge targets of opening bank accounts so as to give a boost to the financial inclusion campaign in the country. All the bank employees were involved to make the program a success. It was followed by demonetisation which made the life of bank employees miserable. Some of them risked their lives while taking cash from one place to another in odd hours, that too without any security provided to them.

It was followed by the wild goose chase by the taxmen at the instance of the government to find out the bankers’ alleged involvement in exchange of banned bank notes with the newly released currency with denominations of ₹500 and ₹2,000. The act of the government was nothing more than a face-saving device and divert public attention from the very fact that 99.5% of the demonetised money had come back to the system and this very fact was revealed by none else than the RBI.

On the other hand, bank employees’ salary hike has been nominal, with merely 2% increase in their pay package offered by the Indian Banks’ Association (IBA) in the wake of fast eroding profitability of banks, thanks to surfacing of a host of mega scams. All of this has demoralised bank employees who feel cheated by those sitting on the corridors of powers. Even in the BoM CMD’s arrest, the bankers’ body, IBA has alleged that the step was ill-advised and that the government has taken the bankers for a ride. Resentment among bankers has grown to such an extent that IBA met on June 21 to discuss the issue.

Taxpayers who have entrusted their money to the government-owned banks should be asking the government to explain why as the custodian of their money, it failed to prevent the fraud

Bankers feel that enforcement agencies are throwing their weight around for entirely petty reasons. Moreover, they blame the government for politically motivated action which is, they feel, the main cause of the current banking woes. The Nirav Modi scam was going on for quite a few years without anyone paying any attention to it. No wonder it went undetected. By the time, the scam surfaced in the media, Nirav Modi had already fled the country and in a classic reply to CBI, he said in a mail that as he was busy with his business, he would not be able to appear before the central agency.

The government has maintained a stony silence on a series of serious allegations levelled by Congress president Rahul Gandhi. Raising concerns about conflict of interest, the Congress President had pointed out that the daughter of Arun Jaitley, former finance minister currently working as a minister without a portfolio, had worked for Nirav Modi. Concerns that the present finance minister Piyush Goyal may also have a conflict of interest since he has been the treasurer of the Bhartiya Janata Party too are yet to be addressed.

Criticising the Modi government on the ₹13,000 crore PNB- Nirav Modi fraud, former RBI governor YV Reddy has slammed the government for its failure to prevent the fraud as an owner of the bank. He has also questioned the functioning of RBI into the matter. The fraud, he went on, is of such a magnitude that it affects the credibility of the RBI in ensuring the trust of people in banking. Reddy maintained that taxpayers who have entrusted their money to the government-owned banks should be asking the government to explain why as the custodian of their money, it failed to prevent the fraud.

Modi Govt has taken measures to strengthen the banking system

It is true that the government has taken a host of initiatives in its bid to make our banking system stronger. It is visible from the measures like setting up of Bank Board Bureau to appoint the top brass in public sector banks and bringing qualified people from outside to function as bank heads. The only disturbing fact is that these measures are yet to show any significant result. The BB has gone through almost complete revamping since then without any reason given by the government. On the issue of delayed appointment of heads of public sector banks, the current finance minister, Piyush Goyal has declared that the mandarins at the finance ministry were working hard to fill up the vacant posts of head honchos of the state-run banks shortly.

One can only hope that these measures by the government will help arrest the otherwise increasing trend of mounting bad loans with the banks. The Parliamentary Standing Committee on Finance headed by Veerappa Moily has asked the Indian Banks’ Association (IBA) to prepare a road map for addressing the issue of mounting bad loans. Nor is it clear if Insolvency and Bankruptcy Code or IBC is the right solution to the ever-increasing menace of bad loans and defaults. Bankers seem to believe that the 180-day resolution plan for NPAs under the IBC was not an adequate window. Also, they have suggested the urgent need for restructuring stressed assets. According to them, referring cases for resolution under the IBC should be the last option.

Join our official telegram channel (@nationalherald) and stay updated with the latest headlines