Demonetisation: A circus, clowns and a silver bullet

Five years after the disastrous demonetisation, the Prime Minister and his Finance Minister—even the fawning media— no longer speak of the ‘Demonetisation Dividend’. There has been none

Two years back, on November 8, at around 8.30 pm, the Prime Minister of India, with his characteristic love for drama, unleashed on the country what he had then claimed was the one silver bullet which would eliminate the triple evils of black money, fake currency, and terrorism.

According to its inventor—for, it was nothing less than an invention—it was a broad-spectrum panacea to end everything that was holding back India from taking off. So sure was this magician of its powers and potency that he asked for a mere 50 days of inconvenience to be borne by the long-suffering public of India. He must have believed in his own rhetoric, because he offered to make himself available at any crossroad of his detractors’ choice and receive the punishment of their choice, in case the measure failed.

A fawning public and a media, which was only happy to suspend even healthy disbelief, fell for the histrionics of one of the greatest actors India has produced. The breaking voice, the tears, the raw emotion, India had seen nothing like it before, even when the country had won its independence. Except for a small bunch of sceptics, practically all those who heard the declaration and the subsequent avowals at Goa and other meetings, were convinced that a clean India was just around the corner.

Then reality stuck, hard. Chaos reigned. People started dying in bank queues and in hospitals unable to pay for treatment; manyears were lost by those who could ill-afford it, standing in the interminable queues in front of ATMs which didn’t have any money or were unable to dispense currency notes for which they were not calibrated; rules and regulations were changed almost by the hour; decisions were taken and rolled back on the fly; rumours flew thick and fast about currency notes that had chips embedded in them which will lead the IT and ED sleuths right into dungeons of ill-gotten hoards of cash and of river Ganges being submerged with discarded currency notes. In short, it was a circus of sorts where the public didn’t realise they were the clowns.

The audacity with which narratives were changed, the unabashed ways in which goal posts were shifted, and the insensitivity with which people were taken for granted beggared belief. The media, instead of calling the bluff, played up the risible parts such as notes embedded with chips.

If demonetisation did nothing else, it did throw the Indian rural and informal economy truly and irretrievably under the bus. As against the 50 days begged for by the Hon’ble PM of the country, it took more than nine months to pump in currency to get the economy back on its wobbly legs again. Necrosis happens in heart muscles when it is starved of blood for a certain amount of time – its muscles die and it can never work with the same efficiency to pump the blood. What happened with the Indian economy was necrosis as a result of 86% of its currency in circulation being withdraw in one fell swoop, with no forethought, no planning, and apparently on a whim.

In these nine months, India’s GDP tanked, and hundreds of thousands of small businesses went bust, and many more millions of people lost their jobs and means of livelihood. Agricultural produce rotted in mandis as there were no buyers. Entranced by the story told to them by a snake oil salesman who dangled the carrot of a clean, corruption-free India, the public grinned and bore the tribulations of living in a cash-depleted economy as they had visions of the evil rich getting their comeuppance and being found out and put behind the bars.

Schadenfreude more than made up for their own angst and anguish. The dreams before them were further embellished with stories of each Jan Dhan account holder getting money apportioned from the surplus RBI would have from the unreturned money destroyed by the scared black-money holders. The purpose of the present exercise is to crunch numbers—available in the public domain—to get a true picture of the outlandish promises made and the stark reality which is now front of us.

Return Of The Specified Bank Notes

Analysing the trend, on 12 December 2016, I had made a prediction in my blog that a minimum of ₹15 lakh crore would be returned to the system. Finally, after eight and a half months, the RBI Annual Report of 2016-17 disclosed that as on 30 June 2017, they had received ₹15.28 lakh crore of SBNs. The latest RBI report of 2017-18 dated 24 August 2018 disclosed that the final tally of SBNs was ₹15.311 lakh crore, which means 99.2% of the SBNs have been returned to the system, shattering, as indicated before, the dreams of windfall gain which the panjandrums in the government and their drum-beaters were talking up during the first month of the demonetisation.

Disposed Soiled Notes Are More Than Sbns

The RBI had disclosed in Parliament that there were 17,165 million pieces of ₹500 (8.582 lakh crore) and 6,858 million pieces of ₹1000 (₹6.858 lakh crore) in circulation on the date of announcement of demonetisation (total Value of ₹15.44 lakh crore and a total volume of 24,023 million pieces).

It is mystifying to note that Table VIII.7 of the RBI Annual Report 2017-18 shows that 20,024 pieces of ₹500 and 6,847 million pieces of ₹1000 were disposed of as soiled notes, i.e. which means if this is also added to the returned SBNs, a total value of ₹16.859 lakh crore was received against the ₹15.311 lakh crore of SBNs said to have been received! An important fact that should not be missed is that during 2016-17, around ₹3.3 crore of SBNs were also disposed of as soiled notes, which is 61% more than the previous year’s SBN figure.

Compartmentalised accounting such as these do raise clouds of suspicion in the wake of the overall figures put out by RBI, as they have been very cagey with explanatory notes on such anomalies.

Fake Indian Currency Notes (Ficn)

Falling for the tales spun by the government about cross-border terrorists and internal terrorists being financed by fake Indian currency notes (FICN), the gullible supporters of the PM parroted this.

One of the reasons such supporters thought that only ₹11-12 lakh crore of SBNs would return into the system could be because of the notion there was a huge overhang of FICN is in the system.

A study by Indian Statistical Institute, Kolkata, had estimated that the maximum FICN in circulation in the Indian economy was only around ₹400 crore. This was willingly overlooked by the powers that be to push the demonetisation narrative as targeting FICN and for eradicating it.

The RBI Annual Report of 2017-18 has unequivocally stated that the processing of SBNs has been completed in all respects.

The Table VIII.9 of the Annual Report gives the total number of FICN detected. The total SBNs detected as FICN during 2016-17 and 2017-18 together shows only 0.81 million FICN notes (amounting ₹58.3 crore) out of the total SBN of ₹15.44 lakh crore. This is a mere 0.0034%!

Even without drastic methods as demonetisation, our banking system and law enforcement agencies together intercept around ₹70 crore of FICN every year. The demonetisation exercise can be compared to burning the manor down to smoke out a single rat!

What galls more is that, despite the claim that the new notes in a different colour and size and have more security features, counterfeits were in circulation within a couple of months. So far, around ₹4.2 crore of counterfeits of the new currency has been detected by the RBI and banks alone. These figures do not include counterfeit notes seized by the law enforcement agencies.

All the evidence points to the conclusion that none of the originally stated objectives were met by demonetisation. No quantum black money which justify all the miseries the Indian public was put to has been found. On the contrary, as most critics of demonetisation suspect, large caches of black money and counterfeit money got laundered, since possibly more than 99.2% of the SBNs have reached the RBI.

Cash Is King

When the government got panned by the learned economists and realisation dawned on them that its original aims were not going to be realised, its spokesmen and sundry votaries changed tack and claimed demonetisation was for making India a cashless, digital economy.

However, if we consider the retail electronic transactions data published by RBI, there has been no dramatic jump in the total electronic transactions post-demonetisation. It only followed the secular growth trend evident since 2011.

The currency in circulation as on 10 October 2018 was ₹19.688 lakh crore, which is ₹1.711 lakh crore more than on 8 November 2016. The monthly withdrawal of cash from ATMs touched ₹2.76 lakh crore in August 2018 from ₹2.20 lakh crore in August 2016, i.e. a jump of more than 25%! The currency to GDP ratio at the end of FY 2017-18 is back to 10.9% from its previous year’s value of 8.8%.

Increase In Income Tax

Soon after the RBI Annual Report 2017-18 reflected the final amount of SBNs returned, Finance Minister Arun Jaitley put out a Facebook post in which he bragged about the increase in income tax payers and number of returns filed and credited these to Demonetisation. Some of the tall claims made by the Minister were as follows:

• In March 2014, the number of Income Tax returns filed was 3.8 crores. In 2017-18, this figure has grown to 6.86 crores.

• The Income Tax collections have increased from the 2013-14 figure of ₹6.38 lakh crore to the 2017-18 figure of ₹10.02 lakh crore.

• The growth of Income Tax collections in the Pre-demonetisation two years was 6.6% and 9%. Post-demonetisation, the collections increased by 15% and 18% in the next two years.

This Facebook post was quoted verbatim by many mainstream media outlets and everyone in unison echoed Jaitley’s assertion that the above figures indicated that the larger purpose of demonetisation to move India from a tax non-compliant society to a compliant society has been achieved.

Let’s check these figures using income tax data recently published on the CBDT website. It is true that the number of returns filed increased from 3.8 crores in 2013-14 to 6.85 crores in 2017-18. But the pertinent question is whether these increased number of returns translated to more actual ‘tax payers’ and more income tax remittance. To understand this, we should analyse the growth of income tax payers and amount of income tax.

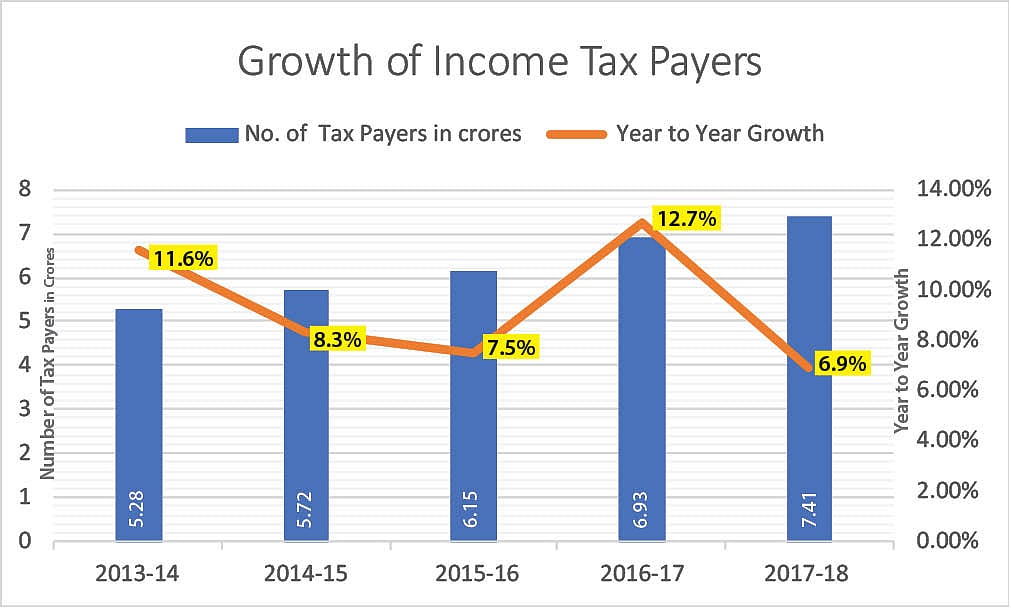

It is evident from the graph (prepared based on CBDT data) that there was an 11.6% growth in the number of income tax payers in 2013-14, without any demonetisation. It then fell to 8.3% and 7.5% in next two years but increased to 12.7% in 201617 but again fell to 6.9% in 2017-18. So, the trend shows that there was no dramatic increase in the number of taxpayers.

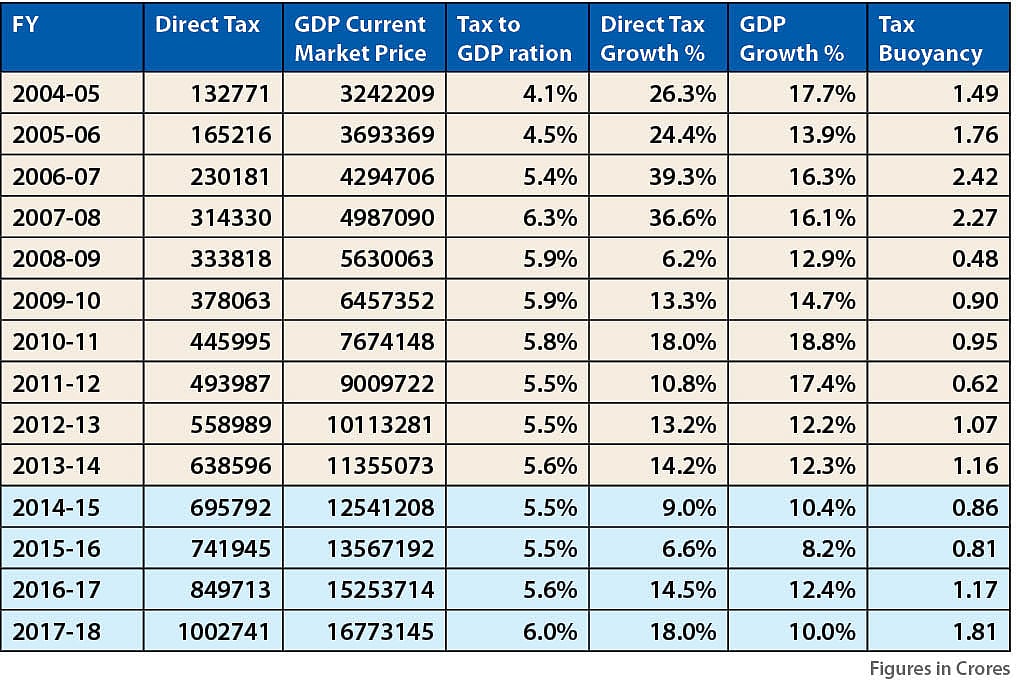

As regards the claim that direct tax realisation has increased from the 2013-14 figure of ₹6.38 lakh crore to the 2017-18 figure of ₹10.02 lakh crore, a glance at the following table prepared from the latest CBDT data will show if the growth claimed is indeed so remarkable.

It can be seen that UPA times, without demonetisation, year-on-year direct tax growth touched much bigger figures. Then, if we look at the Tax-to-GDP ratio, the figures tomtom-ed by the Finance Minister more or less follow the trend for the last 14 years and there is nothing out of the ordinary, despite the demonetisation.

This means figures taken in isolation and blown up do not really reflect the whole picture. Statistics can be used every which way to suit the purpose of the purveyors of such massaged data.

Economists consider Tax buoyancy as an important factor to look for when they compare the direct tax efficiency. It is the ratio between direct tax growth with Nominal GDP growth. It can be seen that, here too, UPA hold the record figures. The average figures of UPA and NDA are provided in the following table, so that the data will speak for themselves. It can be seen that the Direct Tax growth of UPA’s 10 years (2004-14) was an average 20.2% while NDA’s 4 years (2014-2018) have seen only 12%. Similarly, UPA had an average tax buoyancy of 1.33 which is better than 1.17 of NDA.

These should be considered in the light of the fact that the PM came to power on promises to clean up India, to get the tax officials go after defaulters and get in money from all corners. He also used demonetisation to force black money hoarders to cough up their hidden treasures. And yet, despite all the hoopla and song and dance, the NDA government could not match up to UPA’s performance.

A government which believes that repeating a lie enough times makes it a truth should be expected to do worse. That unfortunately is the bane of the country.

This article was first published in the National Herald on Sunday

This article was first published on 04 Nov 2018

Join our official telegram channel (@nationalherald) and stay updated with the latest headlines

- demonetisation

- GDP

- Parliament

- Kolkata

- Indian Statistical Institute

- Specified Bank Notes

- Fake Indian Currency Notes

- Prime Minister of India

- RBI Annual Report