Does RBI's card network flexibility directive quietly promote RuPay?

A Reserve Bank review found some arrangements between card networks and issuers “were not conducive to the availability of choice for customers”

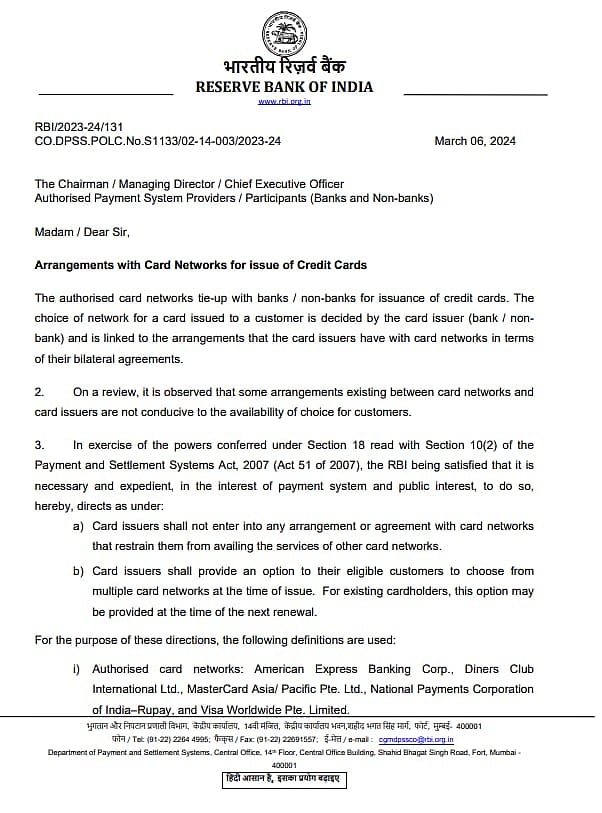

In a directive issued on 6 March, the RBI mandated banks and non-banking financial companies (NBFCs) to offer customers the choice of selecting from multiple networks upon credit card issuance. The directive, effective from 6 September, aims to enhance customer flexibility and choice.

Existing cardholders are also to be given this option upon their next renewal, as communicated by the RBI to banks, NBFCs and payment system providers.

The RBI's decision stems from a review indicating that certain arrangements between card networks and issuers were restrictive to customer choice.

While the regulator emphasised this move as a means to broaden options for consumers, industry observers noted its potential to directly benefit RuPay, the Indian multinational financial services and payment system introduced by the National Payments Corporation of India (NPCI) in 2014. Rupay has issued over 70 crore cards in India already, while dominating the domestic debit card market, according to a July 2023 news report in the Economic Times.

Experts also underlined that this directive does not entail interoperability or portability, but rather, aims to curtail the dominance of global giants like Visa and Mastercard, which together control 90 per cent of the Indian credit card market. The RBI's earlier actions, such as excluding Visa and Mastercard from the UPI network, underscore its strategic alignment towards promoting indigenous systems like RuPay.

The directive prohibits card issuers and networks from entering arrangements that limit customers from accessing services of other card networks. Currently, the network for a card issued to a customer is determined by bilateral agreements between the issuer and networks.

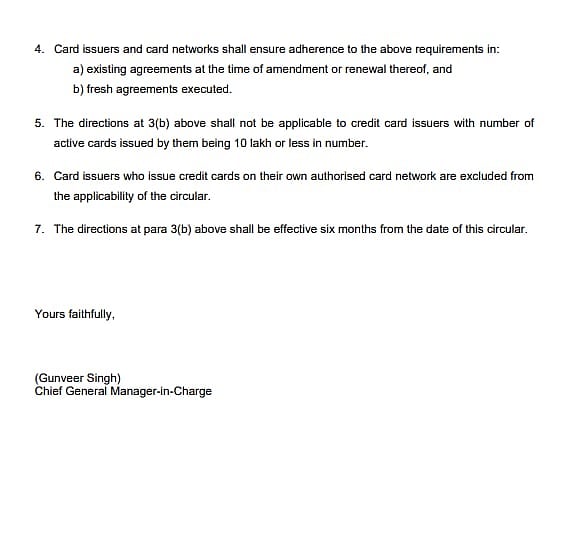

Notably, the directive exempts credit card issuers with 1 million or fewer active cards and those with their own authorised networks. Authorised card networks in India include MasterCard, Visa, NPCI for RuPay, American Express and Diners Club.

India's credit card market has been experiencing robust growth, with the total number nearing the 100 million mark as of December 2023. This trend reflects a sustained push from banks and evolving consumer spending patterns.

Last year, the Reserve Bank of India (RBI) unveiled a draft circular proposing significant empowerment for customers in the credit card market. The draft sought to grant customers the authority to select their preferred card network or issuer. Though initially planned to come into effect from 1 October 2023, the flexibility to seamlessly transition between networks has not been implemented. While the draft circular is yet to be formalised, its implications signal a significant shift in India's credit card market dynamics, potentially positioning RuPay as a formidable player alongside its global counterparts.

Join our official telegram channel (@nationalherald) and stay updated with the latest headlines