The quiet build-up of India’s household debt

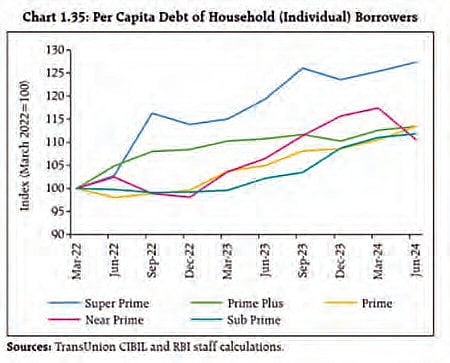

The average debt per individual has jumped 23 per cent in just two years. This means it is rising at twice the speed of national income

India’s households, long regarded as cautious savers, are quietly taking on record levels of debt. According to the Reserve Bank of India’s Financial Stability Report, household debt in India was 42 per cent of the GDP at the end of 2024, up from just 26 per cent in 2015. Which means that in absolute terms, the total debt is nearly three times bigger.

The average debt per individual has jumped 23 per cent in just two years. This means it is rising at twice the speed of national income, from Rs 3.9 lakh in 2023 to Rs 4.8 lakh in March 2025.

More than half of this borrowing, about 55 per cent, comes from non-housing retail loans such as credit card dues, personal loans, auto loans and gold loans, while traditional home loans make up only about 29 per cent of total household debt.

In other words, an increasing share of household borrowing is simply to make ends meet rather than to build assets. Middle-class and lower-middle-class families — known to be thrifty, saving for children’s education or a small home or to buy gold as a financial cushion, are borrowing to spend on current consumption.

A rising debt-to-GDP ratio, especially if the borrowing is driven by consumption rather than productive investment, will weaken India’s prospects of sustained long-term growth. India’s debt ratio is still much lower than seen in developed economies. For instance, in Australia and Canada, the household debt is more than 100 per cent of the GDP.

But unlike India, these two countries have generous social security and assured old-age income security, reducing the need for high savings. In the US too, the ratio of household debt to GDP is 75 per cent and in China, 63 per cent.

Also Read: Why the rupee is plumbing new lows

At 42 per cent of GDP, India’s household debt looks much more manageable than the US — which wouldn’t haven’t forgotten the subprime mortgage crisis of 2007–08 — or China, which has its own chastening memories (Evergrande). But India should be concerned that household debt has risen steadily for five years, substantially outpacing income growth.

A study spanning 54 countries, by the Bank for International Settlements, found that while higher household debt initially boosts consumption and GDP, beyond a threshold of 60 per cent of GDP, it begins to drag down growth, reducing long-run GDP by 0.1 percentage point for every additional point of debt.

India’s ratio, though currently lower, is moving in that direction.

The problem is not household borrowing per se, but the purpose of these loans. Loans for education, housing or small businesses build future assets. But loans for consumption create no productive capacity. As households divert more income towards servicing personal loans and credit card bills, they are left with lower savings or investable surpluses.

The trend has been enabled by easy digital lending, instant credit card approvals and aggressive consumer finance marketing. It has become very easy to borrow small amounts. But the convenience obscures potential vulnerability. A growing number of households are using credit simply to pay for everyday expenses such as groceries, utility bills, school fees or healthcare.

This is seen in the ballooning of gold loans as well. Data from the Reserve Bank of India shows that gold loan portfolios more than doubled between mid-2023 and mid-2025. The growth rate for gold loans was 122 per cent in July 2025! The bulk of these gold loans are worth less than Rs 2.5 lakh, for which the RBI has slackened regulations: appraisal is light and the loan-to-value ratio can be as high as 85 per cent.

Also Read: Beating the 'middle-income' trap

But the RBI is also aware of the build-up of bad loans in microfinance and has tightened regulation there. Microfinance outstandings have dropped 16.5 per cent during the same period, indicating that some of the increase in gold loans is substitution. It means that lower and middle income households that depended on MFIs or unsecured credit are turning to gold loans, which have also been fuelled by soaring gold prices.

The growth rate of gold loans in the next few years is expected to be more than 15 per cent per annum. This is not financial deepening, though; it signals that households are liquidating their last-resort savings to finance consumption or service other debts. The gold loan boom reflects an uncomfortable reality — it is both a safety valve and a red flag.

Alongside rising household indebtedness, two other phenomena are causing concern. Rural wages have stagnated in inflation-adjusted terms. The cost of urban living is rising, and debt has become a coping mechanism. The other worrying phenomenon is the decline in the financial savings of households. Net financial savings have declined from 11 per cent of GDP in FY2021 to just 5 per cent in FY2023. There has been a slight improvement in the past two years.

It’s the household savings pool that support the fiscal needs of governments and the credit requirements of companies. So, a decline in savings implies these will become costlier to finance.

Some of these shifts also reflect a changing credit culture. The aggregate savings rate is down from a peak of 36 per cent to about 30 per cent of GDP. People are aspiring to higher living standards. Digital credit is easy to access, and there is possibly a post-pandemic current to seek instant gratification.

Consumer loans have been outpacing overall bank credit growth for the past five years. Nearly 55 per cent of household debt is non-housing, or essential-consumption loans. Credit card spending has increased 13 times in 13 years, and the number of credit cards in use has quintupled.

Younger, salaried consumers are borrowing heavily against future income to sustain present lifestyles. At the same time, lower-income and rural households, facing stagnant earnings, are turning to gold and small personal loans to manage essential spending.

Credit expansion boosts demand and growth in consumer goods. But it also makes households more vulnerable to the shocks of job loss, illness or crop failure. It crowds out financial savings making credit costlier. Beyond a point, it increases stress in the financial system. Left unchecked, it can erode the resilience of Indian households.

Reversing this slide will require restoring the habit of financial savings, raising real incomes and ensuring that borrowed money builds tomorrow’s assets, not just finance today’s consumption. Aggressive consumer lending needs regulation, and concurrently loans for education, homes and MSMEs encouraged.

India’s households, once the quiet financiers of both growth and government, must be restored to financial health. They need to be encouraged to return to traditional values of caution and thrift rather than pushed down the path of higher debt to financial distress.

Ajit Ranade is a noted economist. More of his writing may be found here

Article courtesy: The Billion Press

Join our official telegram channel (@nationalherald) and stay updated with the latest headlines